We’ve seen you add opportunity filters to your automations to evaluate important criteria such as probabilities, bid/ask spreads, volatility, position count, and more. So, we wanted to improve functionality, streamline the process, and make your automations more efficient by enabling you to set the criteria directly in an open position action.

Great news - you no longer need to add each decision individually. All the entry criteria are available in one convenient location. That’s right, no more friction of adding multiple decisions when building out your scanner automations.

Now you simply check the boxes you want to evaluate, fill in any variable fields, and the bot will automatically reference your settings before opening a position. This simplifies your bot building and makes it easy to modify your opportunity filters quickly.

If you already have entry and position criteria filters in your automations, they will still run as expected, and you do not need to make any changes to existing bots.

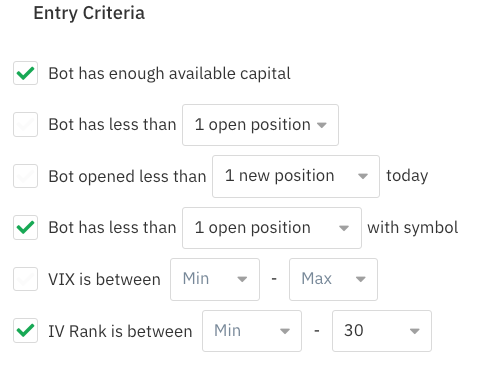

Entry Criteria

The first set of decisions confirms that a potential trade meets your entry criteria before opening the position. The six most common bot-level filters are available:

- Bot has enough available capital

- Bot has less than ‘n’ open positions

- Bot opened less than ‘n’ new positions today

- Bot has less than ‘n’ open positions with symbol

- VIX is between minimum - maximum value

- IV Rank is between minimum - maximum value

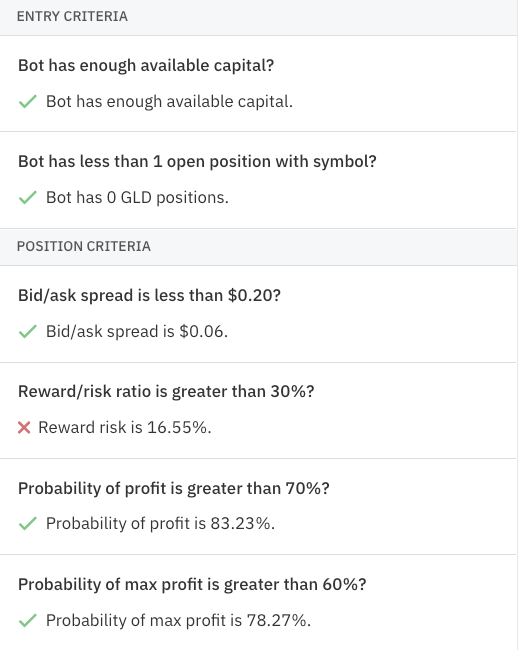

Position Criteria

The second set of decisions checks seven key position-level data before entering a specific trade. We added the most popular opportunity filters:

- Bid/ask spread is less than $

- Mid price is between $ minimum - maximum value

- Expires before next earnings report

- Reward/risk ratio greater than %

- Probability of profit greater than %

- Probability of max profit greater than %

- Probability of max loss greater than %

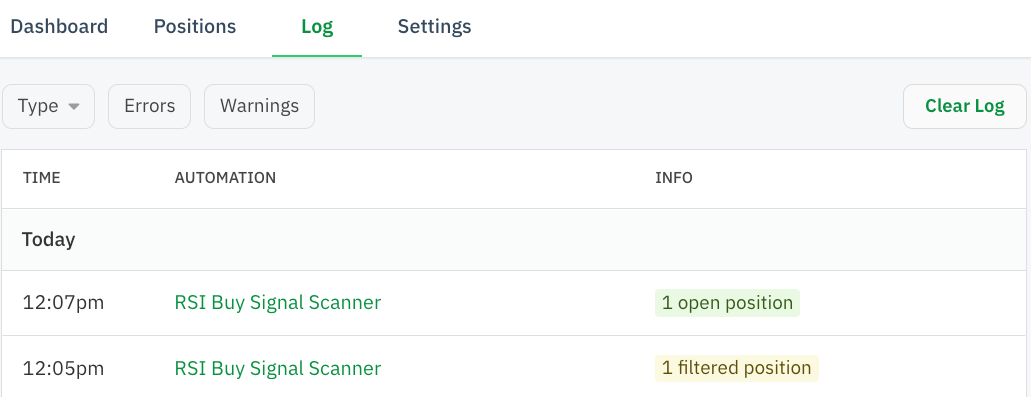

More visible stats in the Bot Log

Bot logs and automation tests display all the bot’s activity and the outcome for each decision, including the new open position action filters.

If the bot cannot open a position, the log shows you which criteria were not met, and the log’s info will highlight a yellow ‘Filtered position’ to indicate the bot did not open the position. You can click on the row to see the automation log and click on the open position action to see the position log’s details.

3 checks your bot now does automatically

In addition to the new criteria checks you can select manually, there are three checks that now happen automatically for every Open Position action.

- Opportunity is available

- Bot can open position

- Bot has no positions with opposing legs

Similar to the 13 new opportunity filters, these automatic criteria checks reduce friction when building your automations. Plus, they'll help you avoid the excessive error failsafe.

The first two auto checks have been available as decision recipes, but the filter now eliminates the need to use multiple decision recipes. The third check filters for "leg stomping" and unnecessary broker rejection errors. Leg stomping could still occur if you have multiple bots in the same brokerage account with the same ticker symbol, strike prices, and expiration dates.

.png)