Options traders often refer to the delta, gamma, vega, and theta of their position as the "Greeks."

Option Greeks are a way to measure an option's sensitivity to ever-changing external factors. Their values are dynamic and fluctuate as price and information changes.

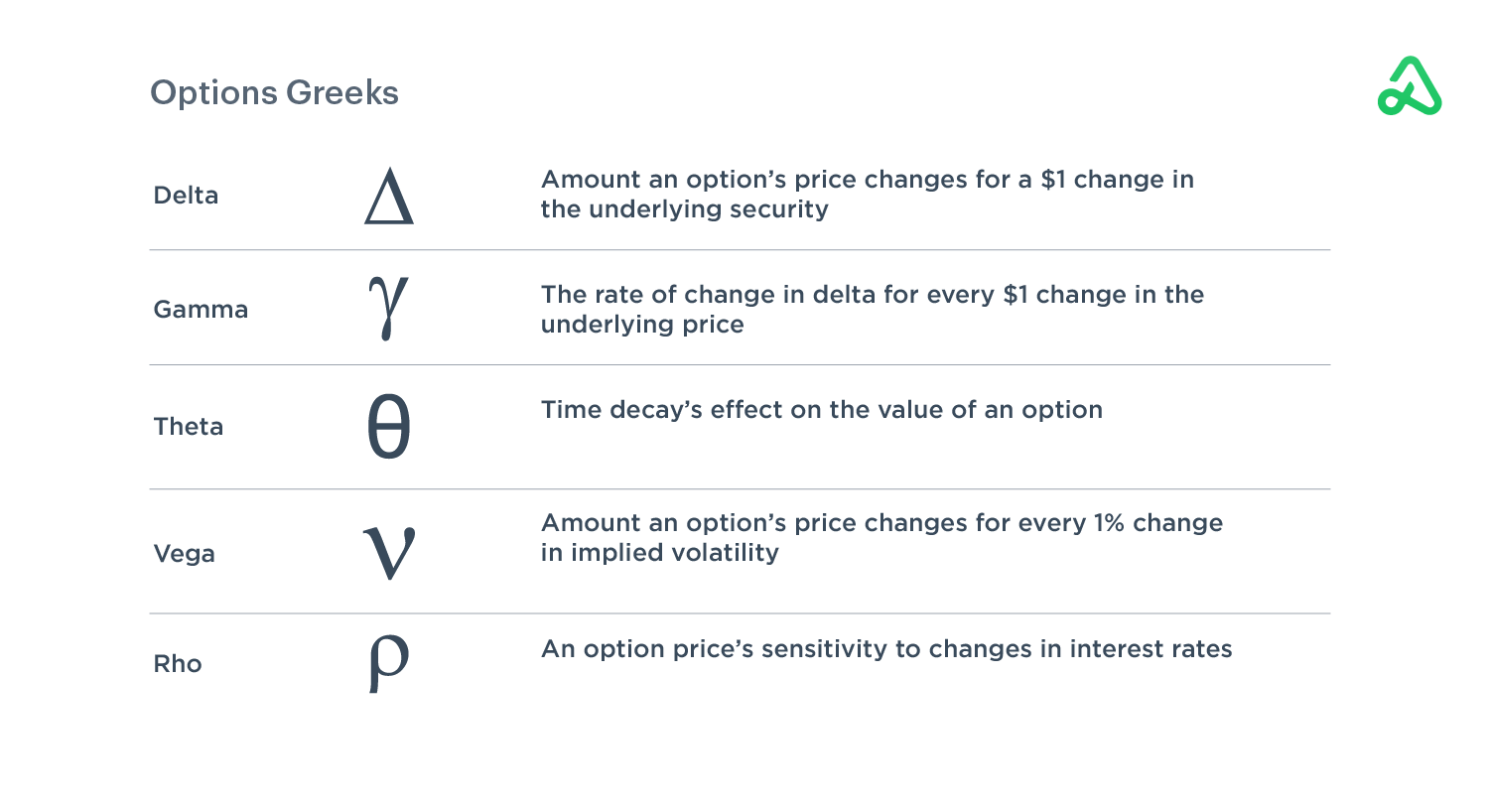

There are many elements to an option’s price. Time until expiration, implied volatility, changes in the underlying asset’s price, and interest rates all impact the value of an option. There are five main option Greeks, and each relates to either the option’s intrinsic or extrinsic value.

Delta and gamma are dependent on the underlying security's price and the option's strike price. Theta, vega, and rho are determined by time to maturity, volatility, and interest rates, all of which are components of extrinsic value.

Delta

Delta is the amount an options price should change based on a $1 move up in the stock.

Calls have a positive delta between 0 and 1, while puts have a negative delta between 0 and -1. Delta would represent the number of relative shares you would own if you purchased an option at a specific delta. Buying a call option with a .50 delta is roughly equivalent to owning 50 shares of stock (and vice versa with put options: -.50 delta is the same as shorting 50 shares).

For example, a stock priced at $100 has a $110 call option expiring in 60 days with a delta of .30 and costs $2.00. If the underlying stock moves up to $101, the option should now be worth $2.30. Owning 100 shares of the stock would have realized a gain of $100. The .30 delta option realized approximately 30 shares worth of value, or $30. Delta can also act as an approximation of the probability an option will finish in-the-money. A .30 delta has roughly a 30% chance of expiring in-the-money (or a 70% chance of expiring out-of-the-money).

Gamma

Gamma is closely related to delta. Gamma is the rate of change in delta for every $1 change in the underlying price. Gamma represents the acceleration at which an option's price increases or decreases. Think of gamma as the next dollar move.

For example, if an option has a delta of .40 and a gamma of .20, the first dollar move in the underlying asset will see the price of the option change by $0.40 ($40). The subsequent dollar move of the stock will see the price of the option change another $0.40 ($40) plus an additional $0.20 ($20). Therefore, a $2 move in stock price will result in a total net change of $1.00 ($100) in the option’s price.

Gamma is higher for contracts closer to at-the-money and more sensitive to changes in the underlying asset price. Gamma risk is the concern that price changes in the underlying asset will have an adverse impact on the option premium. Gamma risk increases as options approach expiration because a small move in the underlying security will significantly impact pricing due to the lack of time remaining on the contract.

Theta

Theta represents the effect time decay has on the value of an option. Options are a decaying asset. Options contracts lose value daily from the passage of time. The rate at which options contracts lose value increases exponentially as options approach expiration. Theta is the amount the price of the option will decrease each day. For example, a theta value of -.02 means the option will lose $0.02 ($2) per day.

Theta is always represented in negative terms because the portion of an option’s value related to time is always going down. Theta value is smaller further away from expiration and is not constant -- it accelerates more rapidly the closer it gets to expiration. Theta is an advantage for the option seller and a disadvantage for the option buyer.

Vega

Vega is the amount option prices change for every 1% change in implied volatility in the underlying security. Vega represents an unknown element because future volatility cannot be predicted. All other components of an option’s price can be determined objectively: spot price, strike price, and time to expiration. Vega has no impact on the intrinsic value of an option. It is not based on price movement in the stock, only changes in volatility. As volatility increases, an option’s price increases as market participants anticipate an above-average move may be possible before expiration. Vega decreases as it approaches expiration because there is less time for volatility to occur.

Rho

Rho measures the sensitivity of an option’s price as it relates to changes in interest rates. Rho represents the expected change of a contract’s value for a 1% change in interest rates. Rho is not as important for short-term options traders because changes in interest rates are usually relatively small, and only adjusted once per quarter, if at all.

Long-term options, or LEAPS, are more significantly impacted by changes in interest rates because of their long expiration period. Investors hedging long-term positions with options may also consider rho, as changes in interest rates will affect the value of those positions.

Transcript

The text is the output of AI-based and/or outsourced transcribing from the audio and/or video recording. Although the transcription is largely accurate, in some cases, it is incomplete or inaccurate due to inaudible passages or transcription errors and should not be treated as an authoritative record. This transcript is provided for educational purposes only. Nothing that you read here constitutes investment advice or should be construed as a recommendation to make any specific investment decision. Any views expressed are solely those of the speaker and should not be relied upon to make decisions.

In this video, we are going to go through Options Pricing and The "Greeks." Now, I can tell you honestly that this is one of my favorite parts about trading.

I'm just a numbers guy by nature and I can tell you that this is by far the number one distinguishes between those people who are successful in this business and those who aren't is understanding how options are priced, understanding the Greeks, how implied volatility and time decay and all of that stuff impacts an options price.

Because if you understand that, then you'll understand where we get our edge in trading. We are going to be going over this a little bit more in some other video tutorials further down in track 1, but today we're going to dive deep in options pricing so that you guys have a clear understanding of it.

So first of all, trying to predict what will happen to the price of a single option or a position involving multiple options as the market changes can be difficult as an undertaking.

So, it's hard, it's easy with stocks right, as you know what's going to happen with the value of the stock because you can see it visually right? The stock value goes up, or the stock value goes down.

With options, there are so many different components that factor in. It's hard to understand that sometimes what is impacting that value of that option.

So if we said because the option price does not always appear to move in conjunction with the price of the stock, it's important to understand what factors contribute to the price of an option and the effect that they have.

Options traders often refer to delta, gamma, vega and theta of their options positions. This is collectively called the "Greeks, " and they provide a way to measure the sensitivity of an option's price to quantifiable factors.

Now, it's really important that you realize immediately that the Greeks do not determine to price and this is a big misconception that people have. Greeks don't determine to price; they just reflect what could happen in option pricing changes for moves in stock, implied volatility, time, etc. Okay!

So Greeks are forward-looking, they are not a determinant of options pricing. They tell you that if this happens then, the price of the option should go down or up by X. Okay?

So they are like little levers, so if you push this level, then you'll get this reaction, if this happens in the stock you'll get this reaction and it's a big misconception that some people have.

So again, before we talk about the Greeks, let's dive a little bit deeper into the overall options pricing which builds on the concepts that you already learned earlier in this course and track 1. All right, so here's the deal.

In the way that I always think about it is like this and this is what we created here for you guys is that options pricing so the price of the option is broken down into couple different categories and then we'll kind of go further and deeper into the Greeks.

Now, we've already talked about intrinsic verses extrinsic values. I think we did that in our last video or the previous video. Inside of track 1 here, talking about in the money, out of the money and at the money options but basically, you can break down the option into two broad components, and that is intrinsic value and time value.

Intrinsic value again being the value of the option right now if it were to be at expiration so does it have any value right now based on the spot price or the stock's price and your strike price.

Meaning if you have a 50 strike call option, so your strike price is at 50 and the stock right now is at 55, you know that you have 5 dollars of intrinsic value in that option right now because you can buy it at 50 and immediately sell it at 55.

Okay? So that's the first component in option pricing is this intrinsic value and again that's just simply looking at the difference between the stock price and the strike price whether you're at the call side or the put side.

Now the other component of options pricing is time value. Now, this is the one that always trips people up. Most people get intrinsic value but this time value aspect has a lot to do with how options pricing fluctuate in addition to the movement of the underlying stock.

Because we know that the intrinsic value is going to move as the value of the stock of the value goes up and down. That's just the straight linear relationship but they extra component here this time or extrinsic value that's a little bit different.

So, that factors in things like time to maturity so how long is it before expiration. Typically options that have a long time before expiration are more highly valued because there is a long time for that contract to be out there. Options that have a low time until expiration are typically lower valued, all things being equal.

Volatility! Again this is the key right here. I can tell you right now, if you've watched any of our videos here or if this is the first video that you are watching here at option alpha, I am telling you right now that volatility is the key to everything that we do here as a trader and trading options.

It is the number one most important thing that you can master and volatility, when it comes to options pricing just basically means that when the markets are more volatile so when there's high volatility then option pricing is high as well across the board.

Calls, puts, everything on both sides when there's high volatility, options pricing goes up as well because a rising tide raises all ships meaning that when the markets are very volatile and swinging back and forth wildly, then each strike price has a better chance of being hit.

When volatility is low or dropping, then options pricing, as a result, goes down and when markets are low in volatility means they are just moving sideways and not making those huge moves like a high volatile market.

In low volatility markets like that, the option pricing is low because then those further out of the money strike prices don't have a high chance of being hit. The market just doesn't move all too much. Then the last thing that effects the value of an option is the rate of interest or interest rates.

This is rho. We don't usually talk about this one but briefly cover it right here, but we don't usually talk about this kind of like the mane for Greeks and Rho effects options that are far out end dates.

So just like time to maturity and just like volatility, as of contract expiration is further and further out, we're talking six months a year two-three years out then interest rate impacts will have a bigger impact on the value of that option.

For what we do here at option alpha and what most traders do, trading inside of 60 days, the impact of interest rates is nonexistent almost. So, we don't cover it as a kind of main Greek, but it is there just so you guys know.

Okay, so that's kind of like the basics for options pricing. Now let's dig a little deeper into the actual Greeks, and we'll relate this back to the things we just talked about. So, again options pricing broken down into those two main categories, then all the ones below now we have the Greeks, okay?

Again, we have the four major Greeks: Delta, Gamma, Vega, and Theta and then we have Rho which is the interest rate one as well, okay! We don't want to discount that, don't want to assume its not there, it is, but it doesn't impact shorter maturity options.

So again, the Delta is now going to give you and show you that relationship for intrinsic value okay. This is basically what Delta does. It gives you the relationship that how much money you're going to make for that particular strike price based on any particular movement in the underlying stock and again we'll go over each of these individually with a lot of examples too, okay.

Gamma doesn't have a connector here, but Gamma is related to Delta. So gamma is considered primarily, the rate of change or the acceleration amount of delta. So basically it shows you that next dollar amount, how much more are you going to make that next dollar and then the next dollar and then the next dollar.

Vega is very easy to remember. Vega and Theta are very easy to remember because I always think V-Vega, V for Volatility. So, Vega is going to tell you what the impact is on that option for a one person change in volatility.

And again, all things being equal, what happens to the value of that option should volatility go up or down by one percent. T for Theta is time to maturity. This is going to tell you how much the value of that option decays every single day as it gets closer to expiration.

Remember, options are wasting assets. As they approach expiration the Theta decay as its called or the time decay starts to accelerate as it gets closer to expiration, time is running out, the clock is running out, and so the value of the options go down dramatically as we get closer to expiration.

And then again we have Rho which is the rate of interest, okay. So let's go a little bit deeper here and talk a little more about Delta, and we'll go through Delta, Gamma, Theta, and Vega and go through some cool examples using some live pricing at the time I'm doing this video.

Hopefully that helps kinda clear things up for you guys. So, lets talk about Delta. Delta is one of the biggest ones you'll probably hear. We talk about it here generally, not to often, but we will talk about Delta a lot, and you'll see it on your local platform.

Now Delta is the amount an option price is expected to move based on a $1 move up in the underlying stock. Now the key here is that the Delta is always based on an upward movement of the stock. It's always based on a $1 move no matter if it's a $500 stock or a $2 stock, it doesn't matter.

It's always based on a $1 move and a $1 move up. Now naturally then, call options have a positive delta, between 0 and 1 meaning that if the stock moves up that is always good for wrong call options and then vice versa.

Put options always have a negative delta between 0 and -1. That doesn't mean that they are bad, it just means that when the market is moving up, then it negatively effects Put options. But, when the market moves down by a $1 then it would positively impact a Put option okay.

So that's the text book definition if you will think of Delta. Let's dig deep here and look at some examples. So this is my live broker platform. Right now we are looking at GDX. Why GDX, because I just typed it in and then we're just looking at it okay.

The stock right now is trading, live trading at 20.60 okay, this is ETF for gold. So, it's live time trading at 20.60, and I've got two contract months open. I've got April expiration, and I've got the May expiration.

April expiration has about 24 days to go, and May expiration has nine days to go okay. So this going to help us to show the differences of how these numbers are going to shift and change and move as we go further out into expiration or closer into expiration okay.

And then again we have the weekly contracts that are in between here as well. All right, so let's go in here and start looking at some Delta's. One of the first things I want to do is I want to look at these 21 strike call options for both April and for May expiration.

Again, I am just highlighting it here so you can see it a little bit more clearly and focus in on it. But, inside of our platform or at least something or in most broker platforms you have all the different groups here: Delta, Gamma, Theta, Beta and you can change these things.

Again, we are working on just the call side right now. Now remember, Delta is going to tell us how much money we make or lose based on the $1 move up in the stock.

So right now, the Delta of the 21 strike call options is 46.46 and what this means is that if the stock goes $1 higher from where its at right now, so from 20.62 to 21.62 all else being equal, all things else being equal, then this value of this option contract is going to go up by $46.

And the current value of this contract is about $74. This is a big spread here. So, its currently valued at $74 so if the stock goes up by $1 then this option contract should go up by $46, okay.

So again, we can see the impact that Delta has. It gives you a barometer for how much money do I make for every $1 move up in the stock.

Again now, as we look out towards the May expiration, you can see that there is a bigger impact in May for the same underline move because there's a little bit more time left until expiration.

So again, still the same $1 move up in the stock from where it is right now, 20.60 up to 21.60. That gives you a $49 increase in the value of the option okay. Those options out in May are a little bit more expensive because of a bunch of different factors which we will continue to talk about.

But those options have a lot more time decay, a lot more volatility baked in and are going to profit a little bit more from a quick move up in the underline stock. They cost more upfront, but they're going to profit a little bit more, couple dollars more, for a $1 move up in the stock.

Okay, so that's on the call side. Now, let's look on the Put side of the trade at the same 21 strike Puts. So the same 21 corresponding strikes but now on the Put side and you can see here for Delta that all of the Delta's are negative.

Now that doesn't mean that you're always going to lose money, it's just remember that Delta is telling you how much money you make for $1 move higher in the underlying stock. If you owned the April 21 strike Puts and the stock moved up by a $1, the value of your contracts would go down by 54 cents.

So right now they're valued at about a $1.12, $1.13, they would go down by $54. Now, that also means that in reverse you would make money so if the value of GDX went down by $1 instead of up, if the value of GDX went down from 20.60 to 19.60 then you would make $55 okay.

So just the complete opposite. If the value of the stock goes down with Put options, then you make this Delta which is 0.55 okay. On the call side again the same relative thing is going to happen here.

You can see the Delta is -51 on the 21 strike Puts for May. That means the value of GDX the stock itself goes up by a $1 or lose $51 and if it goes down by a $1, we make $51. Okay, so hopefully you can see how that relationship starts to interact with each other.

Now one thing that I want to point out is that obviously, the value of in the money options is always going to have a higher Delta than out of the money options okay.

And again remember that Delta is more of your intrinsic part of options pricing and basically bakes in the intrinsic value of those options that are already existing meaning how much money could you make if the expiration was today, and you can see that any options that are on the money both in the call and put side, any options that are for the money have higher Delta's whether they're higher negative or higher positive.

They have higher Delta's approaching 1 or negative 1 which is parity with the options. Any options that are out of the money usually have lower Delta's because they're not going to be as responsive to a $1 move in the stock as something that is on the money.

So if you bought a 23 strike let's say call that's way out of the money and $1 move up, it's still not going to be on the money.

So the $1 move up from the stock of 20.60 up to 21.60, you're still not going to have your stock price above your strike price or have an option that's now in the money so that option is going to be less responsive and is going to profit less than something else that is a little bit closer in.

These options are always cheaper, so the market is always fair and efficient with how it prices its options. All right, so let's move on here and talk about Gamma. Now Gamma's a little bit different. Remember, Gamma is going to be related and tied into Delta.

Gamma is the rate if a change in delta based on a $1 change in stock price. Again, so if Delta is the "speed" at which option prices change, or how much you make or lose, and you can think of gamma as the "acceleration." So, options with the highest gamma are the most responsive to stock price changes in the underlying security.

The way that I think about gamma because I know its hard and I'm trying to give you guys as much information as possible. The way that I think about gamma is I think about gamma as the additional profit or additional loss for the next dollar.

That's how I think about it. And so let's go back here to GDX and kind of use an example here okay. So, if we were looking at these options now, and move around here to challenge you here on option pricing.

So if we were looking at the 22 strike call options in April, the delta for these options is 30 right. So let's round that so we have round numbers here. Its 29 something, so that's 30 okay. So that means that if GDX goes up by a $1, the first $1 from 20.56 to 21.56 you make $30 okay.

If it goes up another $1 from there so from 21.56 to 22.56, you'll make another $30 plus the additional $1 is going to get you another $15 a profit. So the first $1 that you make or the first $1 up in GDX you take in $30, the second $1 or $2 higher you take in an additional $45 for that move higher, okay.

So you can see that as the stock rallies your profit potential at least with call options, as the stock does rally in your favor you have an opportunity to kind of compound a profit here in a small snowballing fashion.

Again, it can work in the complete opposite so if the stock moves down by a $1, so again let's use this example here, it works complete opposite.

If the stock moves down by a $1 you lose $30 and if the stock moves down another $1 so now it goes from 20.57 down to 19.57 down to 18.57 then you lost another $30 plus another $15 so now you're losing, even more, money as the stock goes down as well okay.

Now I don't want you to think that it only works in one direction, its a two-sided mark obviously and it works in both directions. And again, the rate of change is just showing the incremental impact of the delta in the underlying stock move.

Now, in this case with gamma, gamma is always positive, and it just means the additional money made or lost. So on the put side if you're looking at say the 22 strike puts if the stock moves down by a $1 you make $71.

Remember on the put side you want the stock to go down and that means we make money. If the stock goes up, we lose $71, but if the stock goes down, we make $71. If the stock goes down by another $1 on top of the first $1, then we'll also make another $71 check, and we make an extra $15 on top of it okay.

So that's how you want to think about that. Gamma is the additional money made or lost for each incremental dollar higher and lower. Now notice, what's really important about gamma is that gamma is always highest when its centered around at the money strikes okay.

So generally speaking gamma's highest when its centered around the at the money strikers. As you go further out on each end notice how gamma goes down. That's because you're getting away from being either in intrinsic value or extrinsic value right.

So that's why gamma is lower at the further extremes because its not going to have as much of an impact on the actual options price which is going to have big impacts is when the options are trading right around its strike price okay. So hopefully that makes sense and hopefully that kind of clears that up.

All right, the next option group that we want to talk about is Theta. Theta is time decay or is the enemy number one for option buyers. On the other hand its usually the option sellers best friend, and there are option sellers here at Option Alpha.

It is one of our best friends to have theta or time decay working to our advantage. Now, theta is the amount the price of calls and puts will decrease every single day as the option approaches its expiration.

Remember, option contracts are wasting assets. They decay in value until they reach their intrinsic value at expiration. That means that every day they are wasting away. I think about it as a bucket of water with a slow drip and slowly over time that slow drip is going to empty the value of those options.

That's why we prefer to be option sellers because of this wasting approach to option selling. So again let's go back here to our GDX example, and we can look at some theta inside of here, and I always do that ... so open up garage bands instead of my marker.

So you can see here that this is theta and again its negative in all cases for all options out of the money, in the money options, everything. Theta is always negative for options because options is always a wasting asset. There's no example of option theta would not be negative.

But remember theta is going to be really small far out because the options have a lot of value as we get closer and closer to expiration, theta speeds up. So just to give you like a really good example of this we can look at a couple of different contracts here.

These are the March contracts that expire in two days from now and you can see that the 21 strike call options have a theta of -4. When I go out to the 21 strike call options on the April contract which have 24 days to go, you can see that those are only losing $2 per day wherein theta of -0.02.

So again this is the every single day decline in the value of the option regardless of what happens in the underline stock because of its getting closer to expiration.

So when I look at these April expiration options and this 21 strike call you can see that every single day no matter what happens this option is losing part of its value, $2 per day to time decay okay.

Again, this is going to happen every single day, and that's going to accelerate and speed up because you can see here as it gets closer to expiration, now its losing $4 a day and probably somewhere in between here around the 17 or so or 10 days you can see now its starting to lose $2 to $3 per day okay.

So that time decay aspect is crucial and you have to understand that if you are trading to close in, that theta decay means that your option neither has to make it or break it.

Its either going to make money or not because if it doesn't, you're going to lose a lot of value from those contracts purely on the decay in the options as they near expiration.

Now the same thing goes on the reverse obviously the further out that you go the theta decay is limited. You can see these options only in May. There're losing just about a $1 a day okay.

That's pretty much the lowest that they can lose and the least amount. That means that the value of these options are going to pretty much hold up until they start getting really under 45 days that's when it starts to speed up.

All right, so the last option Greek that we're going to talk about is Vega. Vega is my personal favorite. I believe that this where we make all our money as an options trader and its understanding the relationship between implied volatility, historical volatility and how options are priced okay.

We'll get deeper into this as we go through our edge training here in a couple of sessions on the beginner track here at Option Alpha. So Vega is the amount that a call or put price will increase or change for every 1% change in implied volatility of the underlying stock okay.

So again its always based on a 1% move up in implied volatility and it shows you how much money you'll make or lose if all else stays the same, everything else stayed the same and implied volatility goes up.

Now, Vega does not have any impact on the intrinsic value of the options because again it can impact the kind of like the further out stretches because it doesn't matter if the stock moves its all based on implied volatility in the market.

So it doesn't have any impact on the intrinsic value of the option and-and only affects the "time value" of an options price. Now that said, IV is the most critical element of an option and the options pricing model because of its the only unknown component.

So when you think about this, okay, the options market knows almost everything to determine the price of an option. So going back to this options pricing chart here, to determine the price of an option we know almost everything.

We know the current stock price, check, we know the strike price about the current stock price. That's a given. So we know intrinsic value immediately. We know how much time is left till maturity, we would know what the interest rates are, right, and the only thing we do not know is how volatile this stock is going to be in the future.

This unknown becomes our edge. This is the one component as I mentioned numerous times before if you've listened to anything we've done here at Option Alpha or read anything that we've published, you know that this is the number one component that you have to understand if you want to be successful at trading.

Because its the unknown and therefore its our opportunity to make money, its our edge in the market. So again all these other factors can determine options pricing except for volatility. So how does implied volatility work?

So basically without getting too much into it in this video because we got a lot of other videos that we can go through. But implied volatility works by assuming how far a stock will move in the future.

So basically what happens is that the options market basically determines its implied volatility or the market participants based on how active and how much they want to price an option or how high or low they want to price it, they determine how volatile they expect the stock to be in the future or the ETF to be in the future.

You can see here down below with GDX back here in November or at least at the time we were doing this video, there was pretty low volatility in the market.

So market participants were not expecting GDX to make a really big move and as a result, over the last, you know a couple of months as it headed toward a really big move, market participants got that part right for a couple of months.

You'll notice they started to shift and change there perspective and you'll see this big jump in implied volatility and this is again is all based on current market participants. Its not based on any necessary you know formula or relationship to the stock price, the expiration or any of these other things.

Its based on how active people are buying, how aggressive they're buying options on either end, how far out they're doing it, the prices that they're paying but you can notice that there is a meaningful jump in implied volatility meaning the market participants expected GDX to be fairly volatile sometime soon in the future and you can see once that jump happened exactly that the GDX basically doubled over in a matter of two months or so from around $10 to around $21.

You can see the market participants fairly and accurately predicted that move. Its this implied volatility factor that is unknown so we don't know exactly what the stock is going to do but we do know that market participants can expect a big move out of stock or can expect a little move out of stock and having high implied volatility basically gives all option prices a higher value, having low implied volatility gives all option prices a lower value.

So going back to our trade tab in GDX, when we look at Vega again which is volatility we again see that Vega is pretty much is constant on both sides and is positive. Because its always looking for that one percent move up in implied volatility okay.

It doesn't just like delta its always looking for a $1 move higher; Vega is always looking at the next 1 percent higher in volatility.

So if we look at again the 21 calls and with a vega of 0.2, if volatility in GDX increased by 1 percent regardless of where the stock moved, regardless if its closer to expiration or not, just a 1 percent move up in implied volatility causes the value of this option to go up by $2.

Now in most cases, volatility moves up by a couple of percents, usually 5 or 10 or 20 percent in a given week. So if we're looking at a 10 percent move in volatility, we're looking at a $20 increase in the value of this value in this option, and nothing else had to happen.

The stock could stay the same, we could be on the same day between now and the expiration as in the same time. Everything else being equal just a rise in implied volatility or the market expecting the stock to be more volatile to be more volatile than before causes an increase in the value of these options.

Now again, just like time decay the value of these options will be more dramatically impacted the further we go out because as we have more time till expiration volatility going higher creates a bigger opportunity for the market to swing into a zone that we could make some money in.

So again if we go back here in GDX and if we're looking at these expiration dates, this is the April expiration date, and this is the May expiration date out here. If the stock market is volatile we only have the option until May, there's not too much time for the stock to swing into profitable range but if we have options all the way out until April we don't have too much time.

If we have time all the way out to the May expiration, you can see that we got a lot more time for the stock to move into profitable range. So in this case volatility is going to dramatically impact those options that are a little bit further out in time okay.

We'll be going through a lot more case studies and looks at volatility especially in the coming up videos when we talk about historical volatilities that happen verses implied because that's really how we kind of gain our edge as option sellers.

Remember that the Greeks like we said before are snapshots in time. What's more important to realize about options pricing, is the impact of future time decay and volatility can have a huge impact on option pricing more so than the underlying position and how it moves.

We've proved time and time again and posted many live training videos that showed where the stock moved completely against us where we did not get the directional assumption right meaning we thought that the stock was going to go lower or higher and we were totally wrong but the impact of time decay and volatility and understanding those components or put us in the position where we could take a profit in the trade even though we had the underlying direction completely wrong okay.

So Greeks are just snapshots, they move every single time the market moves, the Greeks are recalculated and always moving as we get closer and closer to expiration. So I know this has been a long video.

Hopefully it was incredibly helpful to understand options pricing. If you have any comments or feedback, I'd love to know. Add them in the comments box right below this video.

If you love this video and thought it was helpful, please share online and spread the word on social media. Help us help you by getting other people involved in options trading.

It's one of the ways we grow here through organic referrals from people like you. Until next time happy trading.

'%3e%3cg id='Final-Copy-2_2_' transform='translate(1275.000000, 200.000000)'%3e%3cpath class='st0' d='M7.4,12.8h6.8l3.1-11.6H7.4C4.2,1.2,1.6,3.8,1.6,7S4.2,12.8,7.4,12.8z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3cg id='final---dec.11-2020'%3e%3cg id='_x30_208-our-toggle' transform='translate(-1275.000000, -200.000000)'%3e%3cg id='Final-Copy-2' transform='translate(1275.000000, 200.000000)'%3e%3cpath class='st1' d='M22.6,0H7.4c-3.9,0-7,3.1-7,7s3.1,7,7,7h15.2c3.9,0,7-3.1,7-7S26.4,0,22.6,0z M1.6,7c0-3.2,2.6-5.8,5.8-5.8 h9.9l-3.1,11.6H7.4C4.2,12.8,1.6,10.2,1.6,7z'/%3e%3cpath id='x' class='st2' d='M24.6,4c0.2,0.2,0.2,0.6,0,0.8l0,0L22.5,7l2.2,2.2c0.2,0.2,0.2,0.6,0,0.8c-0.2,0.2-0.6,0.2-0.8,0 l0,0l-2.2-2.2L19.5,10c-0.2,0.2-0.6,0.2-0.8,0c-0.2-0.2-0.2-0.6,0-0.8l0,0L20.8,7l-2.2-2.2c-0.2-0.2-0.2-0.6,0-0.8 c0.2-0.2,0.6-0.2,0.8,0l0,0l2.2,2.2L23.8,4C24,3.8,24.4,3.8,24.6,4z'/%3e%3cpath id='y' class='st3' d='M12.7,4.1c0.2,0.2,0.3,0.6,0.1,0.8l0,0L8.6,9.8C8.5,9.9,8.4,10,8.3,10c-0.2,0.1-0.5,0.1-0.7-0.1l0,0 L5.4,7.7c-0.2-0.2-0.2-0.6,0-0.8c0.2-0.2,0.6-0.2,0.8,0l0,0L8,8.6l3.8-4.5C12,3.9,12.4,3.9,12.7,4.1z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e) Your Privacy Choices

Your Privacy Choices