In this episode, we explore how traders can rethink their approach probabilities and risk. We'll break down why markets rarely behave like neat textbook models and why extreme events—black swans—are far more common than standard probability assumptions suggest.

Kirk connects probability, risk, and position sizing into a single framework, showing how traders often overvalue win rate while ignoring other key factors of long-term performance. He explains how edge, drawdown depth, and recovery time determine whether a strategy survives inevitable periods of variance.

Over the years, Kirk has shifted from pursuing high win rates to prioritizing expected value and thoughtful sizing, and he shares how automation can help enforce discipline, reduce emotion, and keep traders aligned with their probability expectations.

Fat tails, black swans, and market assumptions

This discussion goes beyond options trading — it’s about developing a complete mental philosophy for thinking in risk. Kirk introduces a quote attributed to Eugene Fama: “life always has a fat tail,” meaning extreme outcomes are not rare anomalies, but are actually a recurring feature of markets and human behavior. Kirk revisits Fama’s efficient market hypothesis and contrasts its assumptions with the reality of repeated market shocks.

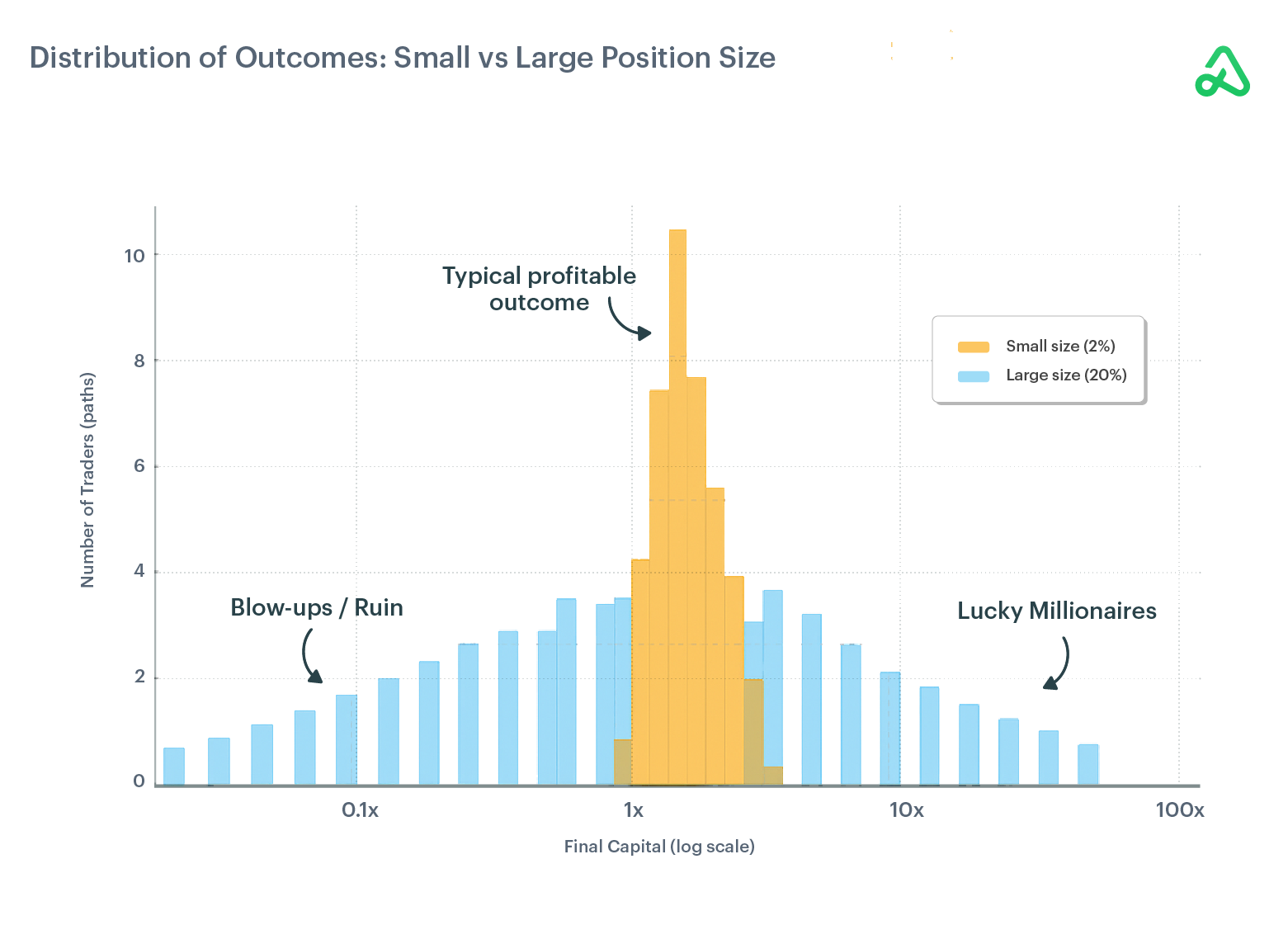

Fat tails invalidate the comfort of models that assume stability and normal distribution. High-probability strategies require small positions because black swan events can cluster, hitting unexpectedly and with outsized force. The real danger in trading is not day-to-day variance but being sized too large when the next fat-tail event strikes.

Probabilities, models, and win rate

To illustrate how probability and risk interact, imagine two traders flipping a coin with the same 50% win rate. One bets 50% of their account per flip, while the other bets 1%. Even though the win rate is identical, the large bettor is likely to blow up after only two losses, while the small bettor survives long enough for the probabilities to play out.

Kirk explains how geometric drag and asymmetric losses damage long-term performance, and he notes that most probability models assume normal distributions simply because there is no better mathematical alternative. Real markets contain far more extreme events than models predict—a theme explored in The Misbehavior of Markets, which documents how events considered “statistically impossible” in theory occur repeatedly in practice.

Because of this, traders must hold cash or cash-like exposure and assume that black swan events will occur. Probability models alone cannot protect traders from extreme outcomes. Trades with marginal edge—like risking $49 to make $51—may look positive on paper but are not robust enough to withstand fat-tail events. Instead, positions must offer large enough expected return to survive both normal variance and the inevitable extremes.

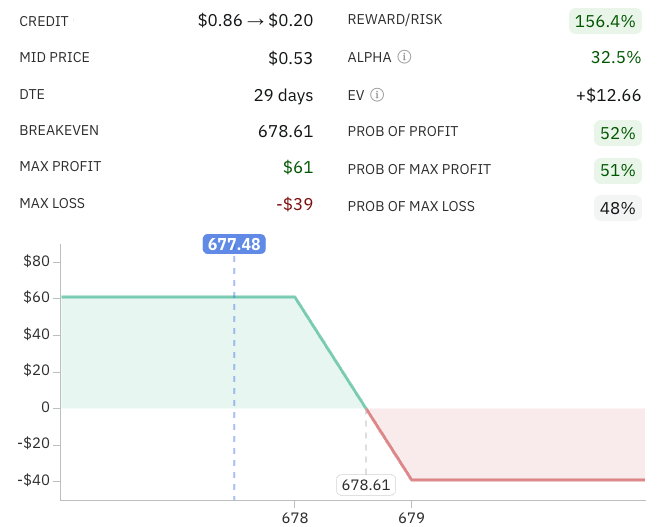

XSP trading example

Kirk demonstrates how probability and risk work together using examples from Option Alpha’s Trade Ideas tool. A short call spread in XSP with a 50% probability of max profit offers a $61 max gain and a $39 max loss. Despite being a coin flip, it has a positive expected outcome.

He contrasts this with an 87% probability short call spread that offers only $12 in max profit while risking $88. Even though it wins more often, it has a negative expected value of roughly –$1 per trade. This explains why traders can experience long winning streaks yet still lose money over time—win rate alone does not determine profitability.

Learn more about how to calculate Expected Value.

Position sizing and recovery time

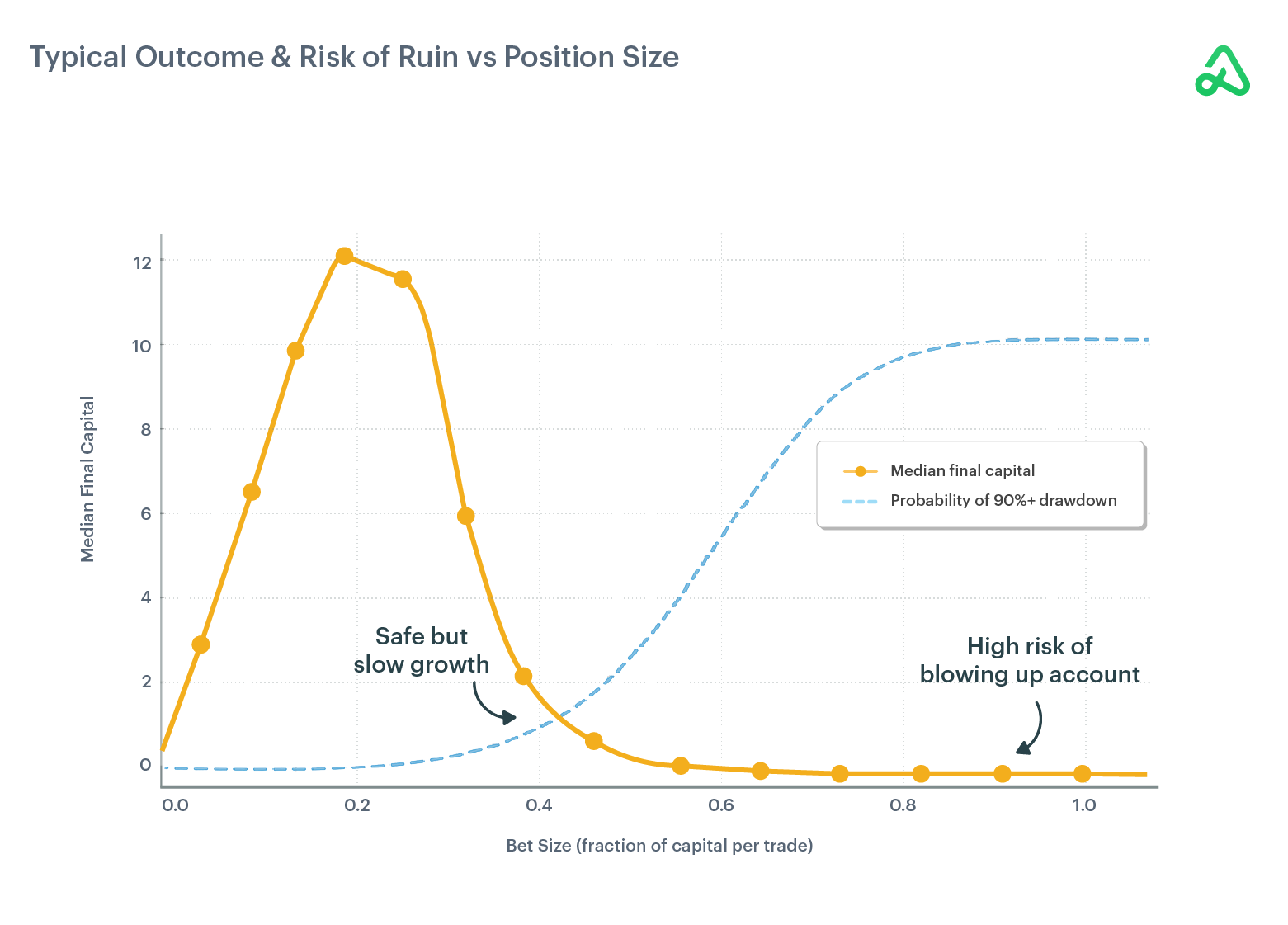

Kirk emphasizes that probability must be evaluated alongside payout and position size. Earlier in his career, he focused heavily on high-probability setups and extremely small sizing. Today, he still sizes small, but with a framework tied to probability and recovery time. He generally sizes trades between ~1% and ~4–5% of the account, depending on the strength of the edge.

Kirk explains why recovery time is just as important as win rate. Strategies with poor risk–reward can create deep drawdowns that require many wins to recover. In contrast, the $61/$39 example has a much shorter recovery path—after seven consecutive losses, only a handful of wins are required to get back ahead. Shorter recovery cycles justify slightly higher allocations on high-edge, mid-probability trades.

Low-probability trades and the psychological side of risk

Kirk also discusses lower-probability setups with around a 20% win rate. These can generate large payouts when they hit, but may go long periods without a win. For that reason, position sizing must remain small so traders aren’t drained by drawdowns.

He highlights the psychological impact of position sizing: losing 0.5% feels manageable, whereas losing 50% in a single trade is devastating. Proper sizing reduces emotional stress and helps traders stick with their systems. Automation further supports this by filtering trades based on predefined probability and reward-to-risk criteria. Kirk uses bots programmed to only take trades with certain minimum edges at specific probability levels.

Misconceptions and key takeaways for traders

Fat tails and black swan events are not hypothetical—they’re a recurring part of market structure. Traders must leave room for the unknown and maintain cash-like exposure rather than going all-in based on model assumptions. Kirk debunks the idea that traders must “bet big to make big,” explaining that large, lucky wins are rarely repeatable and often mask enormous risk.

Automation does not replace traders —i t protects them. It enforces rules, removes emotion, and ensures the consistency needed to survive long enough for probabilities and expected value to work. Kirk encourages listeners to rethink their sizing rules, explore new trade structures in tools like Trade Ideas, and continue refining how they think about risk, reward, and probability.

'%3e%3cg id='Final-Copy-2_2_' transform='translate(1275.000000, 200.000000)'%3e%3cpath class='st0' d='M7.4,12.8h6.8l3.1-11.6H7.4C4.2,1.2,1.6,3.8,1.6,7S4.2,12.8,7.4,12.8z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3cg id='final---dec.11-2020'%3e%3cg id='_x30_208-our-toggle' transform='translate(-1275.000000, -200.000000)'%3e%3cg id='Final-Copy-2' transform='translate(1275.000000, 200.000000)'%3e%3cpath class='st1' d='M22.6,0H7.4c-3.9,0-7,3.1-7,7s3.1,7,7,7h15.2c3.9,0,7-3.1,7-7S26.4,0,22.6,0z M1.6,7c0-3.2,2.6-5.8,5.8-5.8 h9.9l-3.1,11.6H7.4C4.2,12.8,1.6,10.2,1.6,7z'/%3e%3cpath id='x' class='st2' d='M24.6,4c0.2,0.2,0.2,0.6,0,0.8l0,0L22.5,7l2.2,2.2c0.2,0.2,0.2,0.6,0,0.8c-0.2,0.2-0.6,0.2-0.8,0 l0,0l-2.2-2.2L19.5,10c-0.2,0.2-0.6,0.2-0.8,0c-0.2-0.2-0.2-0.6,0-0.8l0,0L20.8,7l-2.2-2.2c-0.2-0.2-0.2-0.6,0-0.8 c0.2-0.2,0.6-0.2,0.8,0l0,0l2.2,2.2L23.8,4C24,3.8,24.4,3.8,24.6,4z'/%3e%3cpath id='y' class='st3' d='M12.7,4.1c0.2,0.2,0.3,0.6,0.1,0.8l0,0L8.6,9.8C8.5,9.9,8.4,10,8.3,10c-0.2,0.1-0.5,0.1-0.7-0.1l0,0 L5.4,7.7c-0.2-0.2-0.2-0.6,0-0.8c0.2-0.2,0.6-0.2,0.8,0l0,0L8,8.6l3.8-4.5C12,3.9,12.4,3.9,12.7,4.1z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e) Your Privacy Choices

Your Privacy Choices