History doesn’t repeat itself exactly, but it often rhymes. The lesson behind Pearl Harbor wasn’t a single mistake — it was quiet concentration. Too many assets in one place. Too much confidence in calm conditions. And when volatility finally arrived, everything was exposed at once.

This episode uses that historical analogy to tell a cautionary story about modern trading portfolios. The danger rarely comes from one reckless trade. Instead, it builds slowly — stacking risk in the same ticker, the same expiration window, or the same type of strategy. On the surface, everything appears diversified. Beneath it, correlation is quietly compounding.

The core message is simple: don’t try to predict the next crisis. Assume volatility will return — because it always does — and allocate capital accordingly.

Understanding the “Pearl Harbor portfolio”

A fragile portfolio doesn’t look fragile in calm markets. In fact, it often looks efficient. Strategies win together. Equity curves rise steadily. Exposure feels controlled.

But hidden concentration risk accumulates when trades cluster around the same underlying, the same duration, or the same market condition. Just as too many ships anchored in one harbor create vulnerability, too much exposure in one corner of the market creates a single point of failure.

The real threat isn’t volatility — it’s complacency during quiet periods.

Are you truly diversified?

Trading only one product — even something highly liquid like SPX — doesn’t automatically mean you’re diversified. True diversification requires exposure to uncorrelated sectors and asset classes: retail, bonds, precious metals, international markets, emerging economies.

Different tickers respond differently to macro shifts. Without that dispersion, portfolios can move in sync during stress events, creating losses that stack instead of offset.

Spreading risk across time

Concentration doesn’t just happen across tickers — it happens across expiration windows.

When too much capital sits in 0DTE trades, a sudden volatility spike can hit everything at once. Short-duration strategies have their place, but anchoring the entire portfolio there increases fragility.

Longer-dated positions — such as 30–45 day trades — distribute exposure across time. They act like ships positioned beyond the harbor, reducing the impact of a single shock.

Diversifying strategy types

Relying on one strategy, even a proven one, creates correlation risk. For example, iron condors and iron butterflies may serve as core tools, but they behave similarly in certain market environments.

A durable portfolio contains strategies designed to win and lose differently. Some benefit from calm markets. Others thrive with volatility. Some are directional. Others are neutral. The goal isn’t complexity — it’s intentional contrast.

Warning signs of hidden fragility

One of the clearest red flags is synchronized performance. When all strategies win together, it feels reassuring — but it also means they may lose together.

Clustered drawdowns are another signal. If losses pile up within the same expiration window or during the same volatility shift, exposure may be too concentrated.

Portfolios that depend heavily on a single market condition — low volatility, steady upward trends, stable ranges — are particularly vulnerable. If a modest volatility spike causes disproportionate damage, that’s not bad luck. It’s structural exposure.

Automation as portfolio radar

Human instinct pushes traders to double down on what’s currently working and abandon strategies that feel slow or underperforming. That tendency increases correlation over time.

Automation provides discipline. By defining allocation rules and guardrails in advance, execution becomes less emotional. Bots act like radar — continuously scanning exposure and enforcing limits even when markets are moving quickly.

Instead of reacting in stress, traders operate within predefined boundaries.

4 practical guardrails for portfolio construction

There are simple structural rules that dramatically reduce concentration risk:

- Limit total exposure to any single ticker to a small percentage of portfolio risk (max 5% total portfolio risk to all open positions)

- Avoid allocating too much capital to a single expiration window (no single expiration window should account for more than 20% of total portfolio exposure)

- Intentionally design strategies to behave differently in changing market conditions

- Regularly ask: What single market shift could disrupt everything at once?

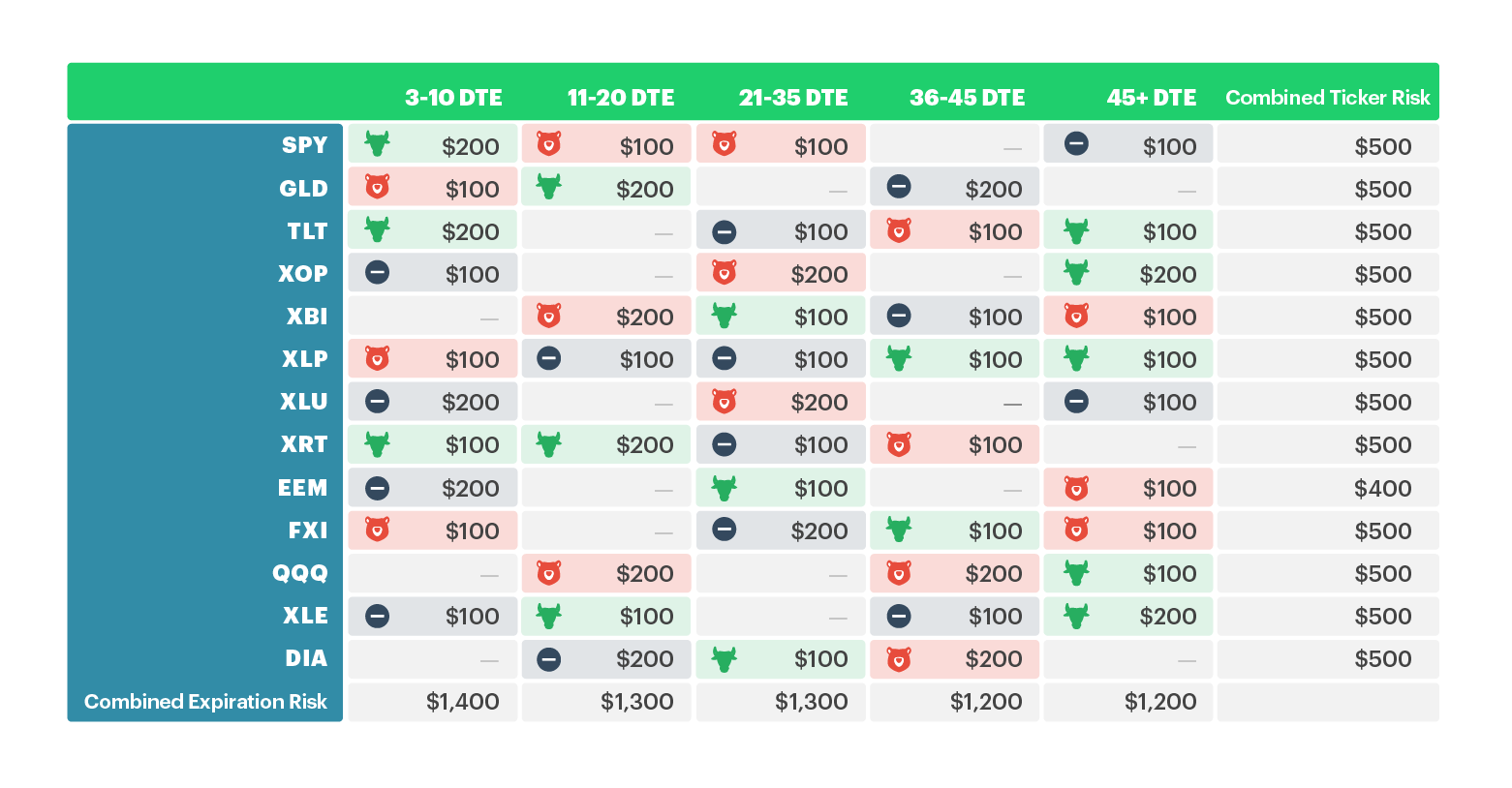

Diversified portfolio example

Here's a look at an example of what a $10k portfolio might look like with diversification across tickers, expiration dates, and strategy types to avoid conentrated risk. No single ticker has more than 5% of cumulative risk, and each expiration period is under 20% portfolio risk. Plus, there is a good mix of bullish, bearish, and neutral positions spread across all trades.

* This image is only an example to help visualize the concepts discussed in the episode and is not a recommendation or financial advice for portfolio management.

'%3e%3cg id='Final-Copy-2_2_' transform='translate(1275.000000, 200.000000)'%3e%3cpath class='st0' d='M7.4,12.8h6.8l3.1-11.6H7.4C4.2,1.2,1.6,3.8,1.6,7S4.2,12.8,7.4,12.8z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3cg id='final---dec.11-2020'%3e%3cg id='_x30_208-our-toggle' transform='translate(-1275.000000, -200.000000)'%3e%3cg id='Final-Copy-2' transform='translate(1275.000000, 200.000000)'%3e%3cpath class='st1' d='M22.6,0H7.4c-3.9,0-7,3.1-7,7s3.1,7,7,7h15.2c3.9,0,7-3.1,7-7S26.4,0,22.6,0z M1.6,7c0-3.2,2.6-5.8,5.8-5.8 h9.9l-3.1,11.6H7.4C4.2,12.8,1.6,10.2,1.6,7z'/%3e%3cpath id='x' class='st2' d='M24.6,4c0.2,0.2,0.2,0.6,0,0.8l0,0L22.5,7l2.2,2.2c0.2,0.2,0.2,0.6,0,0.8c-0.2,0.2-0.6,0.2-0.8,0 l0,0l-2.2-2.2L19.5,10c-0.2,0.2-0.6,0.2-0.8,0c-0.2-0.2-0.2-0.6,0-0.8l0,0L20.8,7l-2.2-2.2c-0.2-0.2-0.2-0.6,0-0.8 c0.2-0.2,0.6-0.2,0.8,0l0,0l2.2,2.2L23.8,4C24,3.8,24.4,3.8,24.6,4z'/%3e%3cpath id='y' class='st3' d='M12.7,4.1c0.2,0.2,0.3,0.6,0.1,0.8l0,0L8.6,9.8C8.5,9.9,8.4,10,8.3,10c-0.2,0.1-0.5,0.1-0.7-0.1l0,0 L5.4,7.7c-0.2-0.2-0.2-0.6,0-0.8c0.2-0.2,0.6-0.2,0.8,0l0,0L8,8.6l3.8-4.5C12,3.9,12.4,3.9,12.7,4.1z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e) Your Privacy Choices

Your Privacy Choices