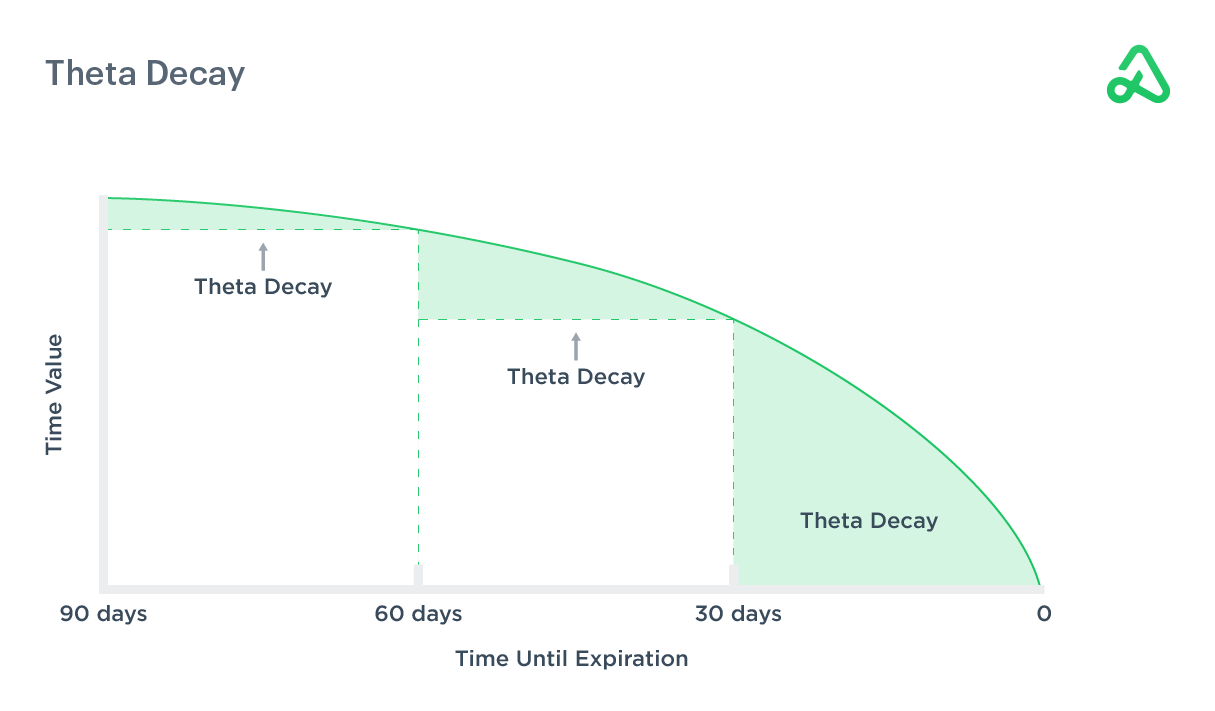

In options trading, the concept of time decay—or theta—is a well-understood phenomenon, particularly over longer durations. Most traders who sell premium (option sellers) specifically target entries and exits to take advantage of the traditional time decay curve.

This video explores the specific behavior of 0DTE options, with a focus on the SPX index. We'll explore the unique decay curve characteristics, analyze empirical data, and discuss the implications for traders.

SPX 0DTE 10 Points OTM Decay Curve

The decay curve for 0DTE options is gradual in the morning, accelerates in the afternoon, and then sharply drops off towards the end of the day, tending toward zero. We observed the most significant price drop typically occurs around 15:30 (3:30 ET), where the spread's value collapses as expiration approaches.

![New 1DTE Options Trading Strategy [Part 2]](https://cdn.prod.website-files.com/5fba23eb8789c3c7fcfb5f31/682651f7b6064584585f2837_Option-Alpha-New-1DTE-Strategy-Part-2-YT-Cover-3.png)

![New 1DTE Options Trading Strategy [Part 1]](https://cdn.prod.website-files.com/5fba23eb8789c3c7fcfb5f31/682651eb03d256edd34a218f_Option-Alpha-New-1DTE-Strategy-YT-Cover-1.png)

%20Bot%20Template.webp)

'%3e%3cg id='Final-Copy-2_2_' transform='translate(1275.000000, 200.000000)'%3e%3cpath class='st0' d='M7.4,12.8h6.8l3.1-11.6H7.4C4.2,1.2,1.6,3.8,1.6,7S4.2,12.8,7.4,12.8z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3cg id='final---dec.11-2020'%3e%3cg id='_x30_208-our-toggle' transform='translate(-1275.000000, -200.000000)'%3e%3cg id='Final-Copy-2' transform='translate(1275.000000, 200.000000)'%3e%3cpath class='st1' d='M22.6,0H7.4c-3.9,0-7,3.1-7,7s3.1,7,7,7h15.2c3.9,0,7-3.1,7-7S26.4,0,22.6,0z M1.6,7c0-3.2,2.6-5.8,5.8-5.8 h9.9l-3.1,11.6H7.4C4.2,12.8,1.6,10.2,1.6,7z'/%3e%3cpath id='x' class='st2' d='M24.6,4c0.2,0.2,0.2,0.6,0,0.8l0,0L22.5,7l2.2,2.2c0.2,0.2,0.2,0.6,0,0.8c-0.2,0.2-0.6,0.2-0.8,0 l0,0l-2.2-2.2L19.5,10c-0.2,0.2-0.6,0.2-0.8,0c-0.2-0.2-0.2-0.6,0-0.8l0,0L20.8,7l-2.2-2.2c-0.2-0.2-0.2-0.6,0-0.8 c0.2-0.2,0.6-0.2,0.8,0l0,0l2.2,2.2L23.8,4C24,3.8,24.4,3.8,24.6,4z'/%3e%3cpath id='y' class='st3' d='M12.7,4.1c0.2,0.2,0.3,0.6,0.1,0.8l0,0L8.6,9.8C8.5,9.9,8.4,10,8.3,10c-0.2,0.1-0.5,0.1-0.7-0.1l0,0 L5.4,7.7c-0.2-0.2-0.2-0.6,0-0.8c0.2-0.2,0.6-0.2,0.8,0l0,0L8,8.6l3.8-4.5C12,3.9,12.4,3.9,12.7,4.1z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e) Your Privacy Choices

Your Privacy Choices